The ‘Great Reset’: How Disney, Netflix, and Comcast Are Diversifying Beyond Subscriber Counts to Win the Entertainment Profit War

The ‘Great Reset’ Has Begun: Why Entertainment Giants Are Abandoning the Subscriber Race

The era of streaming growth at any cost is officially over. Recent financial reports from late 2025 confirm a seismic shift in the entertainment landscape: the Streaming Wars are no longer a subscriber-count competition, but a ruthless Profit War. The major players—Disney, Netflix, Comcast, and others—have entered a ‘Great Reset,’ abandoning the singular focus on subscriber acquisition in favor of robust, diversified revenue streams.

This shift is driven by market saturation, consumer fatigue from fragmented content, and the high cost of content production. The financial pivot is stark: where companies once absorbed billions in losses for market share, profitability is now the explicit, mandated goal. The newest breaking news in this transformation centers on three core strategies: the aggressive embrace of advertising (AVOD), the high-stakes battle for live sports, and the inevitable wave of consolidation M&A.

The New Profit Engine: Advertising and Price Control

For years, Netflix stood as an unyielding fortress against advertising, while Disney’s profitability target seemed perpetually distant. That paradigm has shattered. The 2025 earnings results signal that Ad-Supported Video On Demand (AVOD) is not just an ancillary offering—it is the new financial bedrock of the streaming industry.

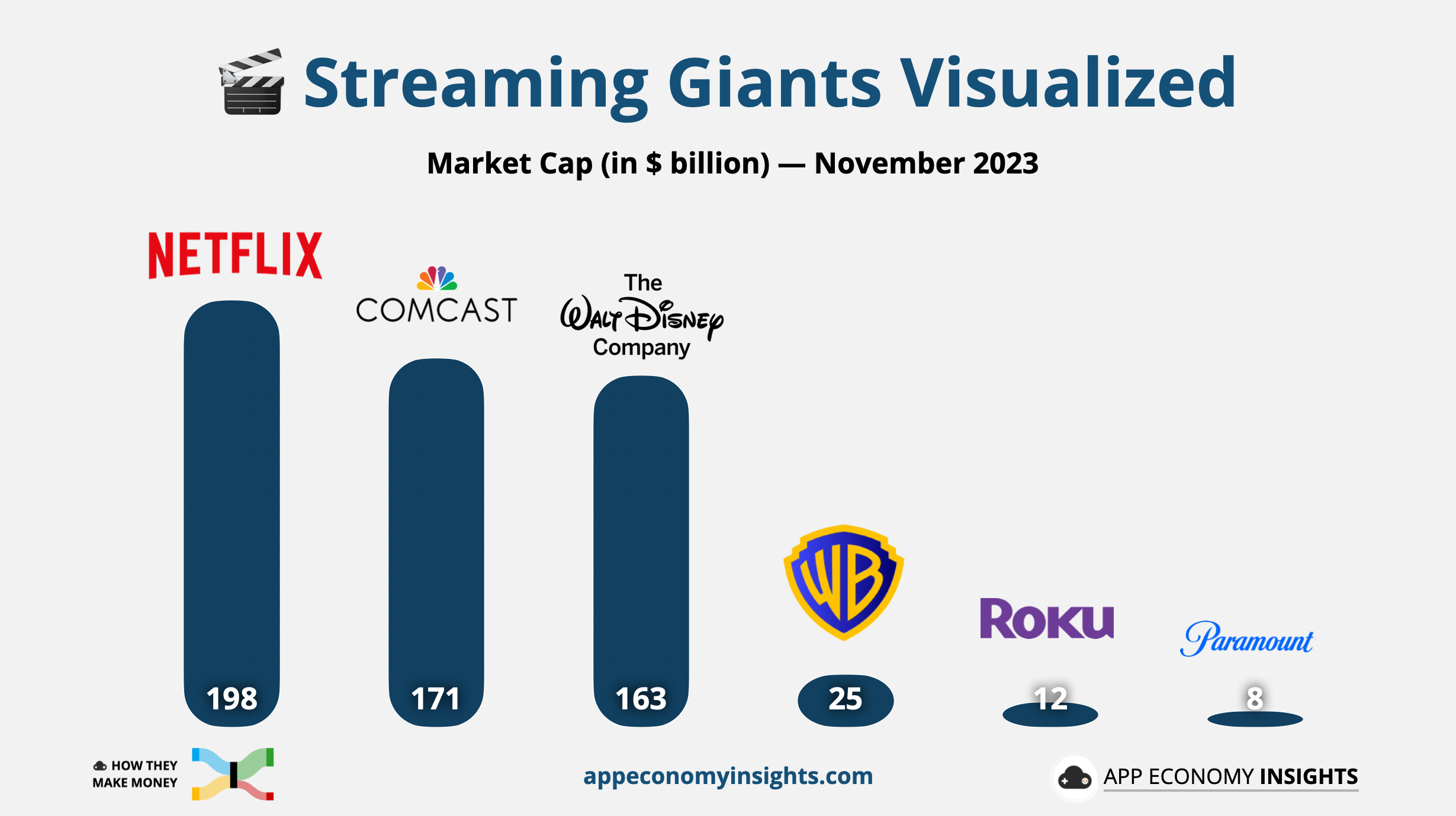

Netflix has emerged as the pioneer, successfully pivoting to profitability through strategic moves that dramatically alter the consumer value proposition. Its crackdown on password sharing and, more importantly, the introduction of the ad-supported tier have proven to be a financial masterstroke. The ad-inclusive tier now boasts an astonishing 70 million monthly active users, driving revenue growth and demonstrating that consumers are willing to trade a little attention for a lower price point. This successful transition allowed Netflix to post profits well over $2 billion in its recent quarter, cementing its dominance.

Similarly, Disney’s streaming portfolio (Disney+, Hulu, and ESPN+) achieved a landmark turnaround, posting its first full-year streaming profit in 2024, followed by continued growth in 2025. This success was powered by price hikes, cost-cutting, and, critically, the success of its own ad-supported plans. The industry is effectively leveraging the difficult economic backdrop to push consumers toward cheaper, ad-supported offerings, which simultaneously boosts top and bottom lines. Global AVOD is projected to expand at a Compound Annual Growth Rate (CAGR) of nearly 30% through 2030, underscoring its long-term centrality to media company diversification.

Crucially, Netflix’s decision to cease reporting subscriber figures in 2025 is the clearest symbolic signal of the ‘Great Reset.’ It shifts Wall Street’s focus from sheer volume to financial metrics and user engagement—a move that effectively declares the first phase of the Streaming Wars (the growth phase) over.

Live Sports: The Ultimate Anti-Churn Weapon

If content drives subscriptions, Live Sports is the nuclear option against churn. The second major pillar of diversification is the aggressive migration of premium, must-watch sporting events from traditional cable and broadcast to streaming platforms. Live sports command a premium, drive immense engagement, and, most importantly, provide compelling, non-skippable content for advertisers.

Recent developments have thrown the battleground into sharp focus:

- The ESPN Pivot: Disney is moving forward with its highly anticipated plan to transform ESPN into a fully-fledged streaming platform within 2025. While facing regulatory hurdles on a joint digital venture with Warner Bros. Discovery and Fox, the intent is clear: to leverage its sports dominance to unlock tremendous value in the direct-to-consumer (DTC) space.

- The New Contenders: Netflix has formally entered the arena, securing rights to live NFL games and high-profile combat sports events, such as the Jake Paul-Mike Tyson fight. Simultaneously, Comcast’s Peacock is leveraging its acquisition of key NBA games to differentiate its offering and drive sign-ups.

- Carriage Fee Battles: The recent breakdown in negotiations between Disney and YouTube TV, a dispute over carriage fees, illustrates that streaming is now the prime battleground for control of this vital revenue stream. The willingness of streamers to ‘flex their muscle’ shows their growing command over audience access.

For entertainment companies, live sports diversification ensures audience stickiness, providing a steady, reliable anchor for a content catalog that might otherwise suffer from cyclical programming lulls.

The Inevitable Consolidation and M&A Wave

The third, and perhaps most immediate, sign of the diversification strategy is the return of high-stakes media Mergers and Acquisitions (M&A). As mid-tier streamers struggle to reach the scale and profitability of the leaders, consolidation becomes a matter of survival, reducing content spend, and increasing market leverage.

Recent speculation centers on Warner Bros. Discovery (WBD), which is potentially on the market. Comcast, the owner of Peacock, is reportedly keen to acquire WBD to combine their two mid-tier streaming services, a clear maneuver to instantly achieve the scale needed to compete with Disney and Netflix. Paramount has also submitted multiple offers for the entire company, highlighting the rush to merge content libraries and subscriber bases. The expectation of a deal by the end of the year suggests a frantic push to rationalize the number of streaming options and improve financial outlooks.

Consolidation offers a three-fold diversification benefit: it reduces operational and content costs, increases the total IP library size for monetization across all platforms, and eliminates a costly competitor, allowing the combined entity to focus on the aforementioned AVOD and Live Sports strategies with greater financial muscle.

Beyond the Screen: IP, Gaming, and Experiential Monetization

For legacy studios like Disney, the diversification strategy extends well beyond digital video. The ultimate goal is not a profitable streaming service, but a profitable ecosystem. Disney’s success, which now generates more free cash flow than Netflix, lies in its ability to treat streaming as just one of several distribution channels, prioritizing Free Cash Flow (FCF) and the monetization of its Intellectual Property (IP) across all segments: Parks, Consumer Products, and Content Licensing.

This IP focus leads directly into the growing convergence of Hollywood and the gaming industry. While pure gaming M&A has recently been dominated by private equity and sovereign wealth funds (such as the recent $55 billion Electronic Arts deal), the movement highlights the immense financial value of IP when applied to interactive media. Major entertainment strategics are starting to explore the User-Generated Content (UGC) space (like Fortnite and Roblox), realizing they need a footprint to capitalize on the next wave of engagement and monetization from their franchises. The sale of virtual goods and experiences based on movie and TV IP represents a massive new, diversified revenue stream that can offset any slowdown in traditional streaming subscriptions.

In the Great Reset, a high-value show is no longer just a retention tool for a streaming subscription; it’s a seed for a new video game, a theme park ride, a range of profitable consumer products, and an anchor for an ad-supported tier. The companies winning the profit war are those that view streaming as a necessary utility, not the sole engine of their future.

Frequently Asked Questions (FAQs)

Q: Why is the entertainment industry suddenly shifting its focus away from subscriber numbers?

A: The industry is shifting because the market has reached saturation, making sustained, high-volume growth financially unsustainable. The priority is now profitability and Free Cash Flow (FCF). Companies spent years building subscriber bases by operating at a loss; now that those bases are established, the focus is on maximizing the average revenue per user (ARPU) through price hikes, ad-supported tiers (AVOD), and diversifying revenue streams outside of core subscription fees.

Q: What is the most significant new revenue stream replacing pure subscription growth?

A: Advertising-based Video On Demand (AVOD) is the most significant new revenue stream. With platforms like Netflix achieving 70 million monthly active users on its ad tier, and Disney also posting significant streaming profits due to ad-supported plans and bundling, advertising is providing a crucial, high-growth revenue stream that reduces customer acquisition costs and increases profitability.

Q: How are live sports changing the streaming landscape?

A: Live sports are becoming the essential anti-churn content. Unlike scripted shows, which can be binged and canceled, live sports like NFL and NBA games require constant, reliable access, driving engagement and providing premium inventory for advertisers. The move by Disney to create a dedicated streaming ESPN service and Netflix’s entry into live events highlight its value as a non-negotiable diversification pillar.

Q: What M&A activity is expected as the OTT market matures?

A: Consolidation is heating up, particularly among mid-tier services. There is significant speculation regarding Comcast (Peacock owner) potentially acquiring Warner Bros. Discovery (WBD) to merge their streaming assets, which would create a larger, more formidable competitor against Netflix and Disney. This consolidation is a direct response to the need for scale and reduced content spending.

Q: How does diversification extend beyond streaming video (e.g., gaming)?

A: Diversification is heavily focused on leveraging Intellectual Property (IP). For companies like Disney, this means monetizing content through theme parks, consumer products, and increasingly, gaming. Major studios are seeking a greater footprint in the lucrative video game and User-Generated Content (UGC) space to utilize their characters and worlds in a new, interactive, and high-margin environment, generating revenue that is decoupled from the monthly streaming bill.

This Post Has 0 Comments